flowchart LR

subgraph Italy["🇮🇹 Italy - Supplier"]

A["🍷 <b>Casalforte</b><br/>Invoices in EUR"]

end

subgraph Risk["⚠️ Currency Risk Zone"]

B["📉 <b>EUR/NOK</b><br/>Exchange Rate"]

end

subgraph Norway["🇳🇴 Norway - Market"]

C["🏪 <b>Vinmonopolet</b><br/>Pays in NOK"]

end

A -->|"💶 €500,000<br/>purchase"| B

B -->|"💰 NOK ???"| C

style A fill:#3b82f6,color:white,stroke:#1e40af,stroke-width:2px

style B fill:#ef4444,color:white,stroke:#dc2626,stroke-width:3px

style C fill:#10b981,color:white,stroke:#059669,stroke-width:2px

11 Quantitative Finance: Currency & Treasury

11.0.1 💰 Beyond Sales: Managing Currency Risk

As a brand manager importing Italian wines, you’re exposed to EUR/NOK currency fluctuations. The Quantitative Finance MCP server helps you understand and communicate hedging strategies to your finance team.

This chapter covers the relevant parts for a brand manager — and includes a fun sidebar for your personal portfolio.

11.1 Why Currency Matters for Wine Importers

When Robert Prizelius imports Casalforte wines from Italy, they pay in Euros but sell in Norwegian Kroner. This creates currency risk:

| Scenario | EUR/NOK Rate | Cost in NOK | Impact |

|---|---|---|---|

| Budget | 11.50 | 5,750,000 | Baseline |

| EUR strengthens | 12.00 | 6,000,000 | +250K loss 😰 |

| EUR weakens | 11.00 | 5,500,000 | +250K gain 🎉 |

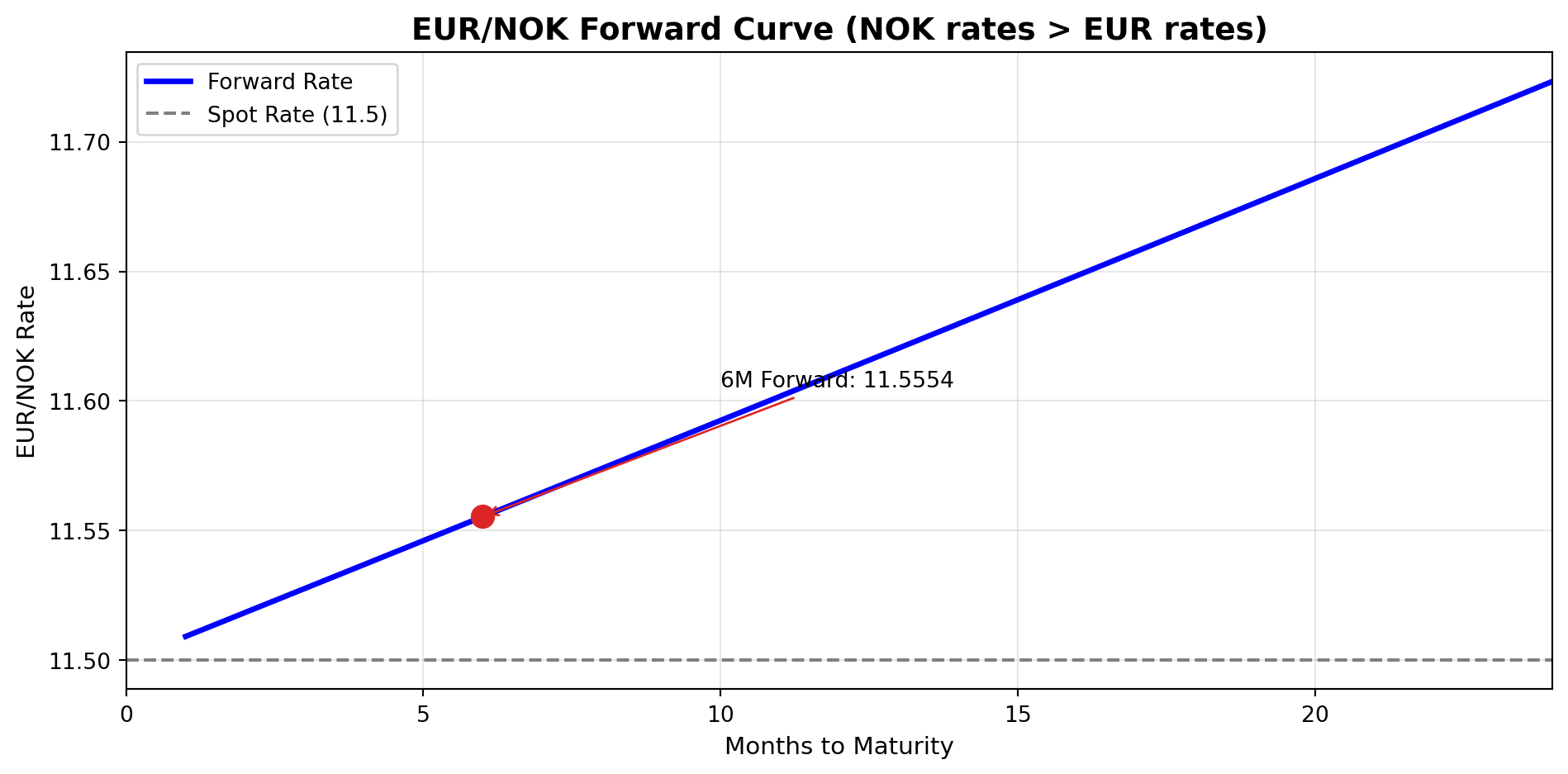

11.2 FX Forward Contracts: Lock In Your Rate

An FX Forward lets you lock in an exchange rate for a future date. This is how professional importers hedge currency risk.

11.2.1 Real Example: Hedging a Wine Shipment

Let’s say you need to pay €500,000 to Casalforte in 6 months:

11.2.2 How the Calculation Works

The Quantitative Finance MCP uses covered interest rate parity:

\[Forward = Spot \times \frac{(1 + r_{domestic})^t}{(1 + r_{foreign})^t}\]

Tip💡 Key Insight: Forward Premium

When Norwegian interest rates are higher than Euro rates (4.5% vs 3.5%), the EUR trades at a forward premium — meaning you pay more NOK per EUR in the forward market than at spot.

This is the “cost of hedging” — but it’s often worth it for budget certainty.

11.2.3 Hedging Decision Framework

| Factor | Hedge | Don’t Hedge |

|---|---|---|

| Budget certainty | Critical for planning | Flexible margins |

| Currency view | EUR expected to strengthen | EUR expected to weaken |

| Margin pressure | Tight margins | Comfortable margins |

| Timing | Known payment dates | Variable timing |

11.3 Interest Rate Analysis: Treasury Management

As a senior brand manager, you might be involved in discussions about the company’s cash management. Understanding bond yields helps you contribute meaningfully.

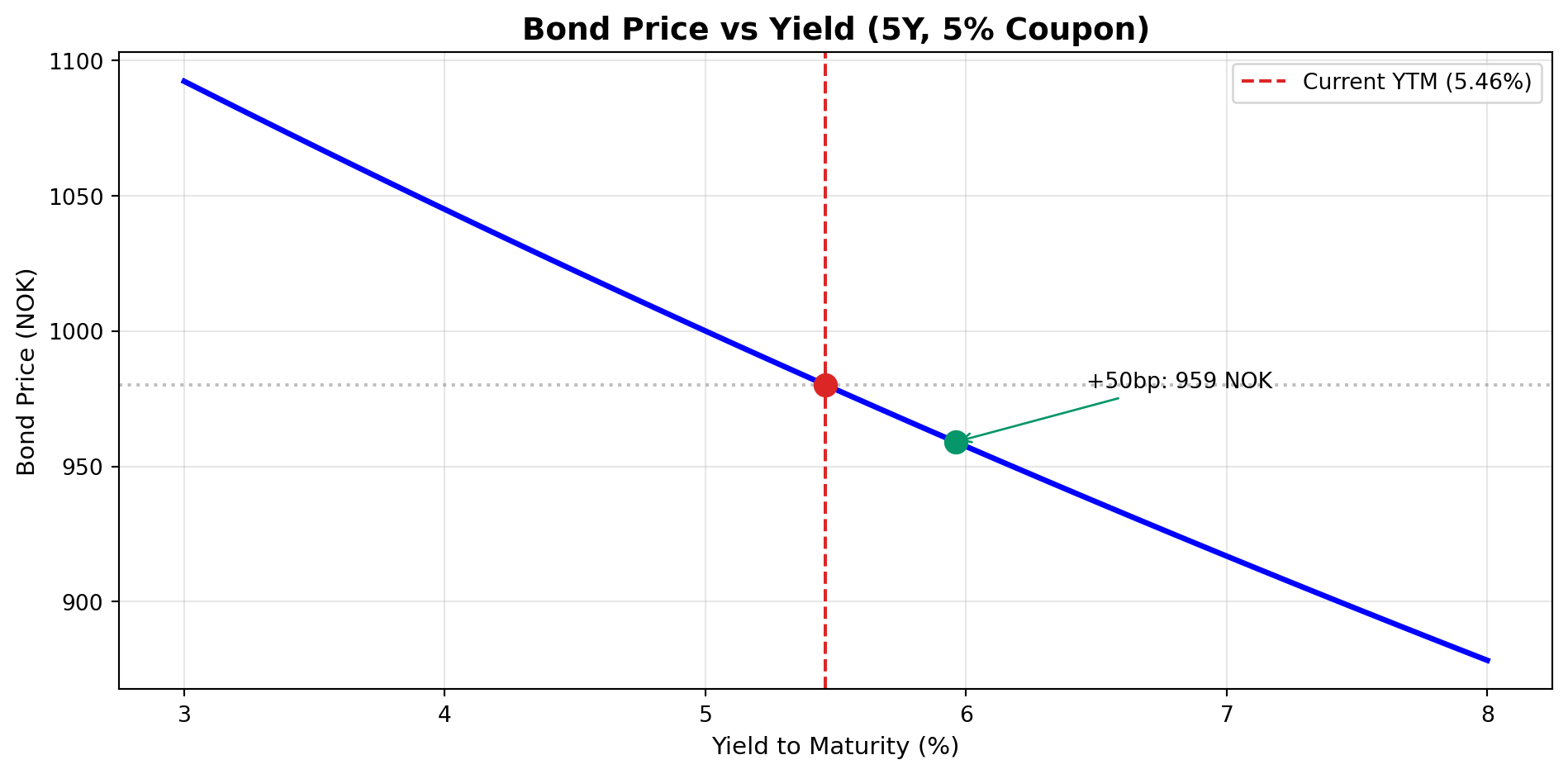

11.3.1 Bond Yield-to-Maturity

If your company holds Norwegian government bonds, you can calculate their true return:

11.3.2 Understanding Duration

Duration tells you how sensitive a bond’s price is to interest rate changes:

Important📊 The Duration Rule of Thumb

For every 1% increase in interest rates, a bond loses approximately duration × 1% of its value.

With a 4.36-year duration: - +0.50% rates → -2.18% price drop - +1.00% rates → -4.36% price drop

11.4 Practical Prompts for Brand Managers

11.4.1 💱 Currency Hedging

11.4.2 📊 Treasury Analysis

11.4.3 📈 Interest Rate Scenarios

11.5 Summary: When to Use Quantitative Finance

| Use Case | Tool | Business Context |

|---|---|---|

| FX Hedging | price_forward |

Lock in exchange rates for imports |

| Bond Analysis | calculate_ytm |

Treasury management, cash allocation |

| Rate Sensitivity | Duration metrics | Understand interest rate risk |

| Budget Planning | Forward curves | Currency exposure in forecasts |

Tip💡 Pro Tip: Speak Finance

Even if you don’t run these calculations yourself, understanding the concepts helps you: - Communicate with your CFO about hedging strategies - Budget with realistic currency assumptions - Negotiate payment terms with suppliers (timing matters for FX)

11.6 What We Didn’t Cover (But You Could Explore)

The Quantitative Finance MCP also includes:

| Capability | Description | Who Uses It |

|---|---|---|

| Options Pricing | Black-Scholes, binomial trees | Traders, quants |

| Portfolio Optimization | Markowitz mean-variance | Asset managers |

| SOFR Swaps | Interest rate derivatives | Treasury teams |

| FRTB Regulatory | Capital calculations | Bank risk teams |

| Model Calibration | Hull-White, SABR, Heston | Quants |

11.7 Next Steps

You’ve now seen how quantitative finance concepts apply to your role. Continue to:

- Chapter 11: Network Analysis — Graph analysis for distribution networks and product relationships